Advertising agencies are under pressure to change archaic and inefficient elements of their business models

IN BUILDING the world’s largest advertising company over the past 30 years, Sir Martin Sorrell, chief executive of WPP, has weathered two recessions and survived a global financial crisis. His firm nearly went bankrupt in the early 1990s. Now he must make his hardest advertising pitch yet, to convince the corporate world that image-making agencies like his are not dinosaurs on the brink of extinction.

The world’s advertising giants are struggling to adapt to a landscape suddenly dominated by the duopoly of Google and Facebook. Some of their biggest clients, such as Procter & Gamble (P&G) and Unilever, are also being disrupted, in their case by smaller online brands and by Amazon. They are cutting spending on advertising services, and also building more capabilities in-house. Consultancies with digital expertise such as Deloitte and Accenture are competing with agencies, arguing that they know how to connect with consumers better, and more cheaply, using data, machine learning and app design.

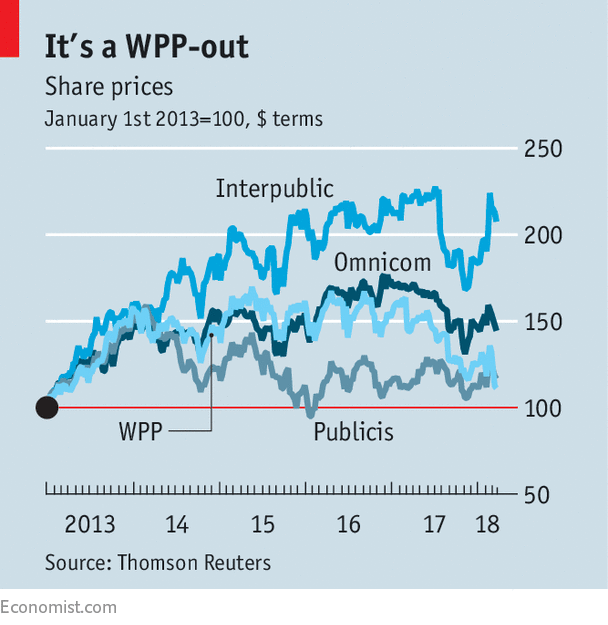

The resulting picture is an industry under siege. WPP just had its worst year since the financial crisis, with declining revenues from like-for-like operations (ie, stripping out revenue from acquired businesses) and a slightly reduced profit margin. This year the company projects that organic growth will be flat, compared with 5% or so in better times. Its big rivals, including America’s Interpublic Group and Omnicom Group and France’s Publicis Groupe, have registered anaemic growth. Publicis posted 0.8% growth in its like-for-like operations in 2017. Investors are losing faith—none more so than WPP’s, who have driven the company’s shares down by 23% since mid-February (see chart).

The ad giants have conventionally made much of their money from huge fixed contracts with clients, which lock in long-term relationships with multiple agencies. Their holding-company structures include famous creative firms that design and make ads for TV and other media, but also a host of other businesses that bring in the bulk of their revenue, such as media-buying operations, digital services, brand consulting and public relations. This month Marc Pritchard, chief brand officer of P&G, criticised their model as a “Mad Men” operation that is “archaic” and overly complex in an era when campaigns and ads need to be designed and refined quickly across lots of platforms.

The ad giants have conventionally made much of their money from huge fixed contracts with clients, which lock in long-term relationships with multiple agencies. Their holding-company structures include famous creative firms that design and make ads for TV and other media, but also a host of other businesses that bring in the bulk of their revenue, such as media-buying operations, digital services, brand consulting and public relations. This month Marc Pritchard, chief brand officer of P&G, criticised their model as a “Mad Men” operation that is “archaic” and overly complex in an era when campaigns and ads need to be designed and refined quickly across lots of platforms.Technological forces are buffeting this model. The first big challenge is disintermediation. Despite the growing backlash against the tech giants, Google and Facebook make it easy for firms big and small to advertise on their platforms and across the internet via their powerful ad networks. The American advertising market grew by around 3% last year, to $196bn, but only because of the tech giants. MoffettNathanson, a research firm, estimates that Google and Facebook each accounted for more than $5bn of growth in advertising spend, and for almost 90% of online ad growth. All forms of conventional advertising, apart from outdoor, shrank.

The second headache is the rise of ad-free content for consumers, especially on Netflix, and the corresponding disruption of ad-supported television, which has declining viewership globally. This hurts agencies because their biggest clients, including the manufacturers of consumer goods, beverages and pharmaceuticals, use television the most. Planning campaigns and creating 30-second spots for television is a people-heavy, high-margin business that the agencies dominate. In America television advertising sales fell by $4.9bn in 2017, or 7.3%, to $62.1bn, according to Magna Global, which is owned by Interpublic. That is the biggest such drop in a non-recession year in two decades.

Third, Amazon’s e-commerce might, and the growing clout of internet-era direct-to-consumer upstarts, have weakened the distribution muscle and pricing power of the advertising giants’ biggest clients. In America Dollar Shave Club, a razor startup, significantly dented the market share of P&G’s Gillette brand in just a few years, forcing price cuts. (Unilever bought Dollar Shave Club in 2016.) Consumer-goods companies are responding to such margin pressure by cutting spending on agencies; P&G has cut agency fees and production costs by $750m in three years, and expects to cut at least another $400m.

Such cost discipline among clients is driven partly by the influence of thrifty private-equity investors like 3G, the Brazilian owner of AB InBev, the world’s largest brewer. It also stems from a perception that the ad agencies have exploited their complexity to boost billings. In 2016 an advertiser trade association issued a report accusing the agencies of using opaque practices, including in digital-ad placement, to extract higher margins. The holding firms strongly disputed the findings, but the report prompted many clients to review their contracts with agencies and insist on more transparency.

Nonetheless, some of the advertising holding companies’ woes may prove less threatening than feared. It is far from clear that Google and Facebook will disintermediate agencies in the long run. The agencies all do programmatic buying of digital ads for clients. WPP, the only holding company that discloses its spending on the two giants, spent about $7bn of its clients’ ad budgets with Google and Facebook in 2017, out of a combined $46bn in advertising sold by both companies that WPP considers agency-relevant business (that is, not counting small-business advertising). Sir Martin says that market share is “not dissimilar” to WPP’s share of ad business with Comcast and Disney.

Spot of bother

Facebook’s recent troubles over data privacy could lead to a regulatory crackdown that constrains both it and Google, potentially opening up the digital-advertising market to more competitors. Facebook’s market share in digital ads in America is forecast to dip this year for the first time. The more options there are for placing ads besides Google and Facebook, the more likely advertisers are to seek the help of agencies.

Sir Martin argues that the budgetary pressures that have forced his clients to cut back on advertising are a cyclical problem, not like the structural challenges posed by technological disruption. He believes that big brands will invest more in advertising to protect their positions in disrupted markets. Some analysts agree with this rosy view. Agency executives further argue that digital consultancies will not be a threat to their core advertising business because they mostly compete for different, lower-cost services.

In private, however, a senior executive at a rival ad-holding firm rejects much of this optimism. Technological disruption and disintermediation, he says, will only deepen. The efficiency of targeted digital ads means companies can spend less for the same outcome in branding.

The advertising firms are responding by hiring away talent, acquiring businesses (in 2015 Publicis bought Sapient, a digital consultancy, for $3.7bn) and gradually changing how they make money. Their plans mostly boil down to two things: investing in digital services and consolidating their collections of businesses so that they can provide a range of services to one client more cheaply under one account.

That should be more than enough to keep them alive. “Everybody says that we’re dinosaurs but we’re not. We’re cockroaches,” explains Rishad Tobaccowala, chief growth officer for Publicis. “We know how to scurry around, we hide out in the corner, we figure out where the food is, we reconstitute ourselves.”

–

This article first appeared in www.economist.com

Seeking to build and grow your brand using the force of consumer insight, strategic foresight, creative disruption and technology prowess? Talk to us at +9714 3867728 or mail: info@groupisd.com or visit www.groupisd.com